Practice sharing III

LATE OBJECTION OF ESTIMATED ASSESSMENT

Overdue objection

Evaluate tax cases

Assessed Assessment

Is it impossible to make an objection after the objection period?

Case sharing

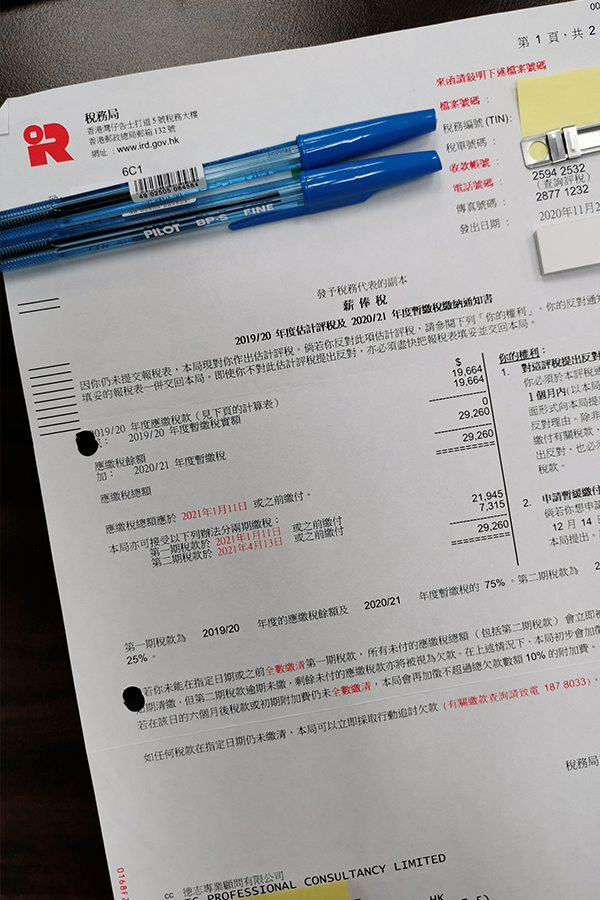

As the guests did not submit their tax returns to the Inland Revenue Department before or after the deadline. The tax bureau will issue the evaluation tax receipt to the guests on November 27, 2020. Because the guest has moved and has not updated his new address to the tax bureau, the guest has not received the evaluation tax slip. Until December 30, 2020, the colleague of the guest also received the evaluation tax form, and the guest found the evaluation tax form after consulting the tax bureau, but the response period has expired. According to the tax regulations and the experience of handling tax by residents, once the objection period (i.e. within 1 month from the date of evaluation of the tax receipt) has passed, the tax bureau will not approve the objection and the objection will not be successful.

In consideration of the guest’s situation, we decided to help him deal with this objection and apply to the Tax Bureau for objection on December 31, 2020 (the objection application has been made after one month’s objection period). Subsequently, the Tax Bureau issued a revised tax assessment form on February 4, 2021, which represented that the objection had been accepted.

The guest was very happy because he did not have to pay the tax specified in the evaluation tax form, but paid the tax according to the income filled in the tax return.

This case shows that the objection made after the objection period may not be unsuccessful. Although the opportunity is relatively low, it can be handled well through some methods.